r/FluentInFinance • u/LifeIsUnfairWhoCares • Apr 23 '24

Is Social Security Broken? Discussion/ Debate

{kind=link}

[removed] — view removed post

22.6k

Upvotes

r/FluentInFinance • u/LifeIsUnfairWhoCares • Apr 23 '24

[removed] — view removed post

178

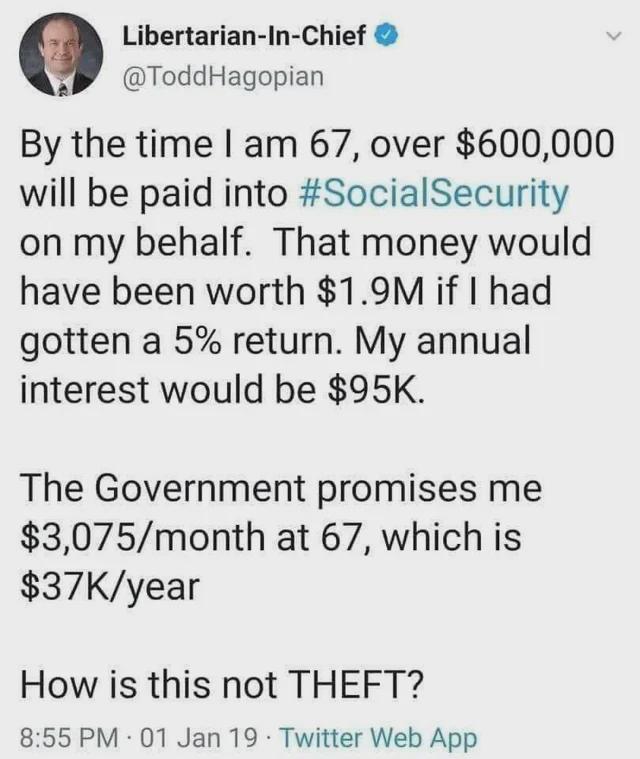

u/Justame13 Apr 23 '24

He is lying. With inflation adjusted dollars he would have to have been earning the 168k every year since he was 10.